The Unbearable Riskiness of Concentration: Big firms in small Nordic Countries

The small Nordic economies are at risk of having all their growth eggs in one basket when a handful of firms account for a hugely disproportionate share of both profits and R&D.

In the early 2000s Finland was the darling of industrial and employment policy analysts everywhere. This small country experienced a high tech-led productivity revolution. Real GDP per capita in local currency terms rose 55% from 1995 to 2007, nearly double the US increase and close to the top of the rich country league list.

Yet spectacular growth abruptly halted after 2008. Real Finnish per capita income actually declined slightly from 2008 to 2019 as the European Central Bank fretted about imaginary inflation and most EU countries opted for austerity to resolve the euro crisis. But an equally large reason was Finland having many of its growth eggs in a single basket: Nokia. Nokia’s handsets and related telephony equipment accounted for 20% of Finnish exports at peak, driving Finland’s current account surplus to nearly 7% of GDP. When the Apple iPhone launched in 2007, Nokia’s handset market collapsed, exports fell by half, Finland’s current account swung into deficit, and a decade plus of economic stagnation began.

All the Nordic economies are exposed to this ‘Nokia Risk,’ albeit less so than other, less well-governed and less-resourced societies. Aside from Iceland, which faces the different risk of volatile raw materials prices, a handful of firms account for a hugely disproportionate share of both profits and R&D in the bigger Nordics. Think Novo Nordisk, Volvo Trucks, or Ericsson. These firms have relatively large shares of cumulative profits over the last decade relative to the universe of firms in both their home country and the world. Their profits largely explain why these small countries have a share of global profit that exceeds their share of global GDP, and, in turn, relatively high per capita income.

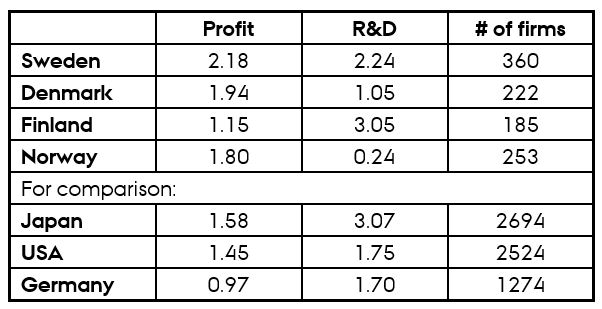

Table 1 shows the ratio of the share of cumulative global profit and of R&D expenditures to country share of global GDP, based on 21,580 global ultimate owners (headquarters firms) with annual sales averaging at least $10 million from 2011 to 2020. The very long tail of small firms excluded here typically depend on the larger firms for their revenue. For example, Danish pharmaceutical giant Novo Nordisk alone accounts for a quarter of cumulative profits for the 200 plus Danish firms in Table 1; its 0.2% share of cumulative profits for all 21,580 firms is almost 50 times the average for that group (as per data from the OECD Economics Department). The actual concentration is even higher: insulin accounts for roughly 7% of cumulative Danish goods exports 2002 to 2021. Insulin and diabetes related products account for 80% of revenues for Novo Nordisk.

Table 1: Ratio of share of cumulative Profit and R&D spending to share of Global GDP, by country, 2011-2020

Source: Author calculation from Bureau van Dijk Orbis database and IMF World Economic Outlook database.

Schumpeter’s business cycles

The influential economist Joseph Schumpeter’s 1939 book ‘Business Cycles’ analyses the dynamic change in capitalist economies and is helpful in shedding light on the economic risks facing the core firms in the Nordic countries. Schumpeter identified four such revolutions that had taken place by then:

(1) The industrial revolution, centering on canals, water mills, textiles, and other household nondurables, with small owner-operated factories collecting handicraft producers under one roof.

(2) In the mid-1800s, a revolution that focused on steam power, railroads, and iron goods, as well as larger but still owner-operated factories using custom-made machinery.

(3) The end of the 1800s saw the rise of large corporations which began to separate ownership and management, and progress that was based on electricity, steel steamships, urban trams, bicycles, and chemicals.

(4) The fourth wave – characterized most famously by Ford – centered on internal combustion engines for land and air transport, petroleum, mass consumption of consumer durables like vehicles, continuous flow-assembly line production, and vertically integrated and often multidivisional firms with full separation of ownership and management.

Since Schumpeter, a fifth – and perhaps even a sixth – phase can be discerned:

(5) The fifth wave began in the US in the 1960s with the development of the semiconductor chip, soon spread globally, and lasts arguably until today. It is based on connectivity via electronics (ICT), negative energy consumption via digitalization, pharmaceuticals and first-generation biotechnologies, software and semiconductors, global supply chains, and de jure vertically disintegrated firms with de facto control by lead firms.

(6) A potential sixth wave is arguably discernable built on artificial intelligence (AI), machine learning (ML), and second generation (CRISPR-cas) biotechnology as general-purpose technologies that threaten leading firms’ existing production systems and markets.

Likely changes to economic landscape will be a challenge

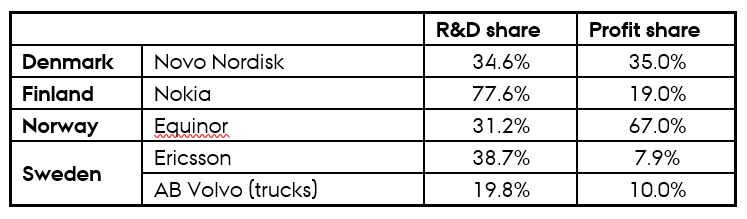

Nordic giants confront two big challenges based on this business cycle model. First, on the economic front, the fifth Schumpeterian growth wave clearly has exhausted much of its growth impulse as sales of its iconic smartphone slow, and a potential sixth wave threatens to undermine Nordic firms’ existing production systems and markets. Second, politically, governments everywhere are ramping up anti-trust and other attacks on visible monopolies, and edging towards more nationalistic industrial and trade policy. Because these firms account for disproportionate shares of their home economy R&D, profits, and exports (Table 2), failing to navigate these challenges will result in a major economic shock for their small, rich home countries.

Table 2: Firm share of cumulative national R&D and profits for high R&D firms, 2004-2021

Source: Author calculation from European Commission data.

Looking to radical innovation in key areas

Joseph Schumpeter’s dynamic change – or creative destruction – required radical innovation in five key, interconnected areas: new transportation modes, new energy sources, new consumer goods, new general purpose production technologies and, though he underemphasized this, new legal organization or governance structures for firms. Dynamic change came from two types of innovation. The first is the classic entrepreneurial ‘invented in my garage’ (or lab) type, while the second type is the more systematic innovation found in corporate labs. These days, the usual ecosystem involves public funding of basic R&D, spun out into small firms who do contract work for the big firms, who then market the resulting product. The key question for the Nordics is whether their current innovation ecosystem could survive the shock of one of these key firms failing.

Although, as the saying goes, it’s wise never to make predictions, especially about the future, we can hazard a few guesses about the shape of the next, sixth, Schumpeterian wave of leading sectors. Several key technologies and industries have already emerged in the energy and transportation space, as well as – albeit with less clarity – the production software and pharmaceuticals spaces. Alternative and renewable energy sources are clearly replacing fossil fuels as the basis for electricity generation and equipment power, including the critical transportation sector. And artificial intelligence plus machine learning appear to be general purpose production technologies reshaping biotechnology (along with the new CRISPR-cas gene editing technology) and the organization of machinery production. There is no guarantee that incumbent Nordic firms will preemptively master these technologies rather than being displaced as Nokia’s core product was by Apple’s iPhone.

Can ‘Nokia risk’ be avoided?

Nordic states are aware of these risks and have committed considerable resources to educating their populations and, in some cases, creating public goods to support key firms. The share of R&D in GDP in the Nordics is almost double the average OECD country, as is the number of full-time researchers relative to population. As an example, recent Danish governments have promoted Denmark as an ‘innovation country’ and stood up a ‘Disruption Council’ in 2017 to support its biomedical and alternative energy sectors. The Danish National Genome Center (Nationalt Genom Center), the National Biobank (Danmarks Nationale Biobank under the State Serum Institute), and the overarching Royal Bio and Genome Bank collect comprehensive diachronic data from Denmark’s health care system. These data in turn are the feedstock for AI and ML driven R&D projects across the entire pharmaceutical innovation ecosystem. While this enables smaller biotech firms to access large volumes of data, Denmark lacks indigenous AI and ML firms that might supply expertise to the entire sector.

Most countries surely wish they had the problems faced by the well-run, rich Nordic economies. But there is no guarantee of success going forward. Politically, all are vulnerable to deglobalization pressure stemming from Covid-19 and rising US-China tensions. Economically, they are vulnerable to radical innovation that might undermine the value of their Intellectual Property Rights portfolios and product lines. If the winner-takes-all nature of the franchise economy continues, the Nordics, like the Red Queen, must run fast simply to stay in place.

A longer version of this article can be found on Phenomenal World, entitled ‘The Nokia Risk: Small countries, big firms, and the end of the fifth Schumpetarian wave’.

Further reading:

- Carlota Perez, ‘Technological Revolutions and Techno-Economic Paradigms.’ Cambridge Journal of Economics 34, 1 (2010) pp. 185–202.

- Charles Sabel and AnnaLee Saxenian. A Fugitive Success: Finland’s Economic Future (Helsinki: Sitra; 2008).

- Dan Breznitz, Innovation and the State: Political Choice and Strategies for Growth in Israel, Taiwan, and Ireland (Yale; 2011).

- Francesco Daveri and Olmo Silva, ‘Not only Nokia: what Finland tells us about new economy growth, Economic Policy’, 19, 38 (2004) pp. 118–163.

- Herman Mark Schwartz, ‘Club goods, intellectual property rights, and profitability in the information economy’, Business and Politics 19, 2 (2017) pp. 191–214.

- Mikkel Hermansen and Valentine Millot, ‘Adapting business framework conditions to deal with disruptive technologies in Denmark’, OECD Economics Department Working Papers, No. 1545, (OECD Publishing: Paris; 2019).

- Robert H. Frank and Philip J. Cook, The Winner-Takes-All Society: Why the Few at the Top Get So Much More Than the Rest of Us (Penguin; 1996).

Links: